SME credit 2026 budget fit

Finding the right SME loan in 2026 means balancing three hard constraints: price, age, and condition. Lenders have tightened their criteria since the post-pandemic lending surge, making it essential to match your business profile with the right product before applying.

Price is no longer just about the headline interest rate. With the OECD noting that overall SME loan stocks remain stagnant, lenders are using AI to price risk more granularly. A business with strong cash flow but a short history might face higher rates than a slower-growing but older firm. Look for platforms that offer transparent APR breakdowns rather than just monthly payments.

Age refers to both the business and the director. Most traditional banks and many fintech lenders require the business to be at least two years old. For directors, the sweet spot is typically between 21 and 65 years old. If your business is newer, you may need to look at invoice financing or merchant cash advances, which often have less stringent age requirements but higher costs.

Condition covers your credit score, debt-to-income ratio, and industry risk. AI-driven lenders now look at real-time bank data rather than just static credit reports. A high credit score helps, but consistent revenue growth is often weighted more heavily. Avoid applying to multiple lenders at once, as each hard inquiry can temporarily lower your score.

As an Amazon Associate, we may earn from qualifying purchases.

The key is to prepare your financials before you search. Clean books and a clear narrative about your growth can often override minor credit blemishes, especially with AI lenders that value trajectory over static history.

Compare the strongest SME credit 2026 options

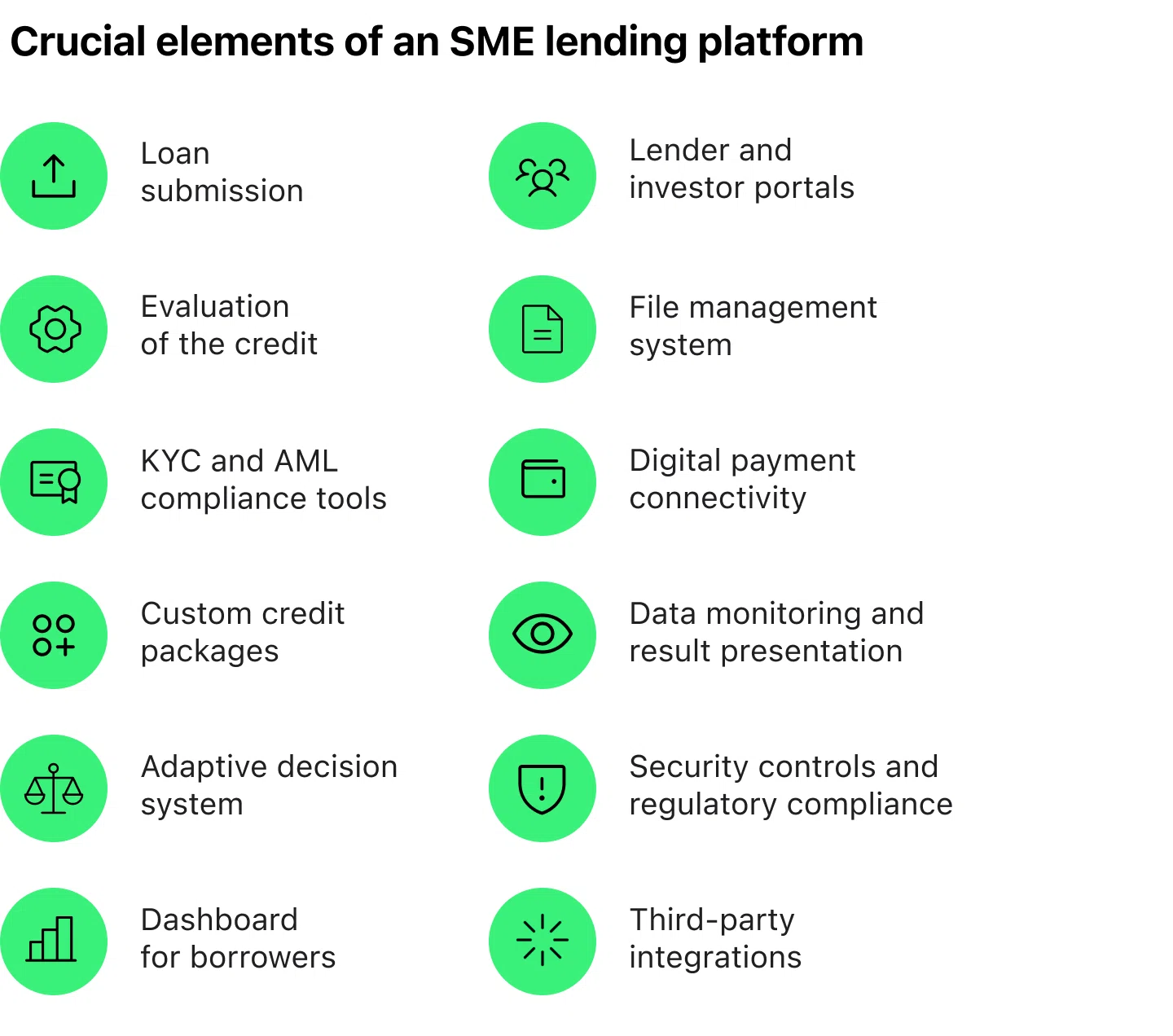

Choosing the right lending platform in 2026 depends on whether you need speed, low rates, or flexible repayment structures. The market has shifted toward AI-driven underwriting, which evaluates cash flow and transaction history rather than just credit scores. Below is a comparison of the leading platforms to help you match your business needs with the right tool.

| Platform | Best For | Approval Time | Key Features |

|---|---|---|---|

| Kabbage | Small, short-term working capital | Minutes | Revolving credit line, automated bank integration |

| OnDeck | Fast term loans | 24-48 hours | Fixed repayments, high credit score requirements |

| Fundbox | Invoice financing and spending control | Same day | Purchase card, real-time expense tracking |

| BlueVine | Credit lines and invoice factoring | 1-2 days | No prepayment fees, up to $250k limit |

When evaluating these options, look beyond the headline interest rate. AI lenders often use dynamic rates that adjust based on your daily sales volume. For example, Fundbox and BlueVine offer lines of credit that are ideal for businesses with seasonal cash flow, while OnDeck is better suited for one-time capital expenditures where fixed repayments provide budget predictability.

The OECD notes that while new lending to SMEs is recovering, the overall stock of loans remains stagnant, making platform selection critical. Use the comparison above to narrow your choices, then check each lender’s specific eligibility criteria regarding turnover and business age before applying.

Inspect the expensive parts

AI-driven lending promises speed, but it often hides structural risks that surface only when cash flow tightens. Before you commit to a platform, run this inspection checklist. It targets the failure points that cost small businesses the most in fees, lost capital, or operational paralysis.

Don’t assume the algorithm reads your bank statements. Many platforms rely on static credit bureau data or third-party aggregators that lag behind real-time cash flow. Ask exactly which data feeds power the decision engine. If the AI can’t ingest your latest payroll or inventory turnover, its risk model is blind to your current reality.

The headline interest rate is rarely the final cost. Inspect the term sheet for origination fees, which can range from 1% to 5% of the loan amount. These upfront costs eat directly into your working capital. A lower rate with a high origination fee often costs more than a higher rate with no fees, especially for short-term SME loans.

AI lenders often lock you into rigid repayment schedules. Check if prepayment penalties exist. If your business experiences a sudden cash surge, you should be able to pay down the principal without penalty. Platforms that penalize early repayment are designed to maximize interest income, not support your liquidity.

Lending platforms require access to your financial accounts. Review their data retention and sharing policies. Ensure your transaction data isn’t sold to third-party marketers or used to train models without your explicit consent. Your financial history is a liability; protect it like one.

Understand the default triggers. AI models can flag minor anomalies as defaults. Know exactly what constitutes a breach of contract. If a single missed payroll date triggers an automatic default, the platform is too rigid for small business volatility. Look for grace periods and manual review options.

As an Amazon Associate, we may earn from qualifying purchases.

Ownership costs: plan for the hidden price tag

A low interest rate is only part of the equation. When evaluating AI-driven lending platforms or the hardware required to support them, you must account for the total cost of ownership. This includes integration fees, data storage, and the ongoing maintenance of the systems that process your loan applications.

Cheap upfront costs often mask expensive operational drag. If an AI lending tool requires constant manual data entry or specialized server upgrades, the savings from lower interest rates vanish quickly. Treat these platforms like infrastructure, not just software. You are paying for reliability and speed, not just access to capital.

Essential tools for streamlined operations

To manage these costs effectively, consider equipping your team with reliable hardware that supports high-volume data processing and secure remote access.

As an Amazon Associate, we may earn from qualifying purchases.

When a cheap buy stops being cheap

The most expensive loan is the one that fails because your infrastructure couldn't handle the volume. If your current systems are outdated, the "savings" from a cheaper lending platform will be eaten up by downtime and inefficiency. Always calculate the cost of switching and integrating new tools before committing to a provider.

Focus on platforms that offer seamless integration with your existing accounting and CRM software. This reduces the need for additional middleware or custom development, keeping your long-term costs predictable and manageable.

Sme credit 2026: what to check next

Before committing to a lending platform or applying for government support, it helps to clarify how eligibility and subsidies actually work in the current market. The landscape is shifting, with AI-driven underwriting changing who gets approved and how fast.

What is the SME subsidy 2026?

The SME Digitalisation Grant 2.0, introduced in the 2026 Budget, provides 50% matching funds up to RM5,000. This subsidy is designed to help Malaysian SMEs adopt digital tools, software, and equipment that improve productivity and competitiveness. It is part of the broader government commitment to accelerating digital transformation across the sector.

Who is eligible for SME loan?

Lenders typically require a minimum annual turnover to assess repayment capacity and operational continuity. Applicants must generally be between 21 and 65 years old. While specific criteria vary by institution, most AI-driven platforms now prioritize cash flow data and digital transaction history over traditional collateral.

How does AI affect SME loan approval rates?

AI models analyze real-time business data, such as bank statements and e-commerce sales, rather than relying solely on credit scores. This allows many SMEs with thin credit files to access capital faster. However, it also means that consistent digital record-keeping is now a prerequisite for approval.

What is the current state of SME lending in 2026?

According to the OECD’s 2026 Financing SMEs and Entrepreneurs Scorecard, new lending to SMEs is recovering but remains stagnant overall. Stability and certainty in capital costs are critical for small businesses navigating this environment. Structural adjustments in lending practices are urgently needed to unlock sufficient capital for growth.

No comments yet. Be the first to share your thoughts!