Why SME credit 2026 matters now

The global financial landscape for small and medium-sized enterprises is at a breaking point. According to the World Bank, SMEs in emerging markets and developing economies face a staggering $5.7 trillion finance gap. This shortfall isn't just a statistic; it is a tangible barrier that prevents millions of businesses from hiring, innovating, or simply surviving economic shocks. While traditional banks remain the backbone of commerce, their risk-averse models often leave viable businesses without the liquidity they need to grow.

This sluggish growth in SME credit is weighing heavily on firm liquidity and investment, with direct implications for global competitiveness, as noted by the OECD. The old methods of underwriting—relying almost exclusively on historical financial statements and collateral—are no longer fast enough to serve a digital-first economy. Businesses need capital when they need it, not after months of bureaucratic review.

SME credit 2026 is the center of gravity because it represents the shift toward data-driven lending. AI-powered platforms are now analyzing real-time cash flow, transaction history, and digital footprints to assess risk. This approach closes the gap between what lenders are willing to offer and what entrepreneurs actually need, turning credit access from a privilege into a scalable utility.

How AI Underwriting Changes Approval Speed

Traditional bank underwriting relies on a rigid checklist: tax returns, credit scores, and years of operating history. If a business lacks one of these markers, the application stalls or fails. AI underwriting breaks this bottleneck by analyzing alternative data points—cash flow patterns, transaction volume, and even utility payments—to build a real-time financial profile. This shift allows lenders to assess risk based on actual performance rather than historical paperwork.

The result is a dramatic compression of time. Where legacy banks might take weeks to underwrite a loan, AI-driven platforms can approve SME credit 2026 applications in minutes. This speed is not just a convenience; it is a lifeline for businesses that need working capital to seize immediate opportunities or cover unexpected cash flow gaps. The "center of gravity" for modern lending has moved from static documents to dynamic data streams.

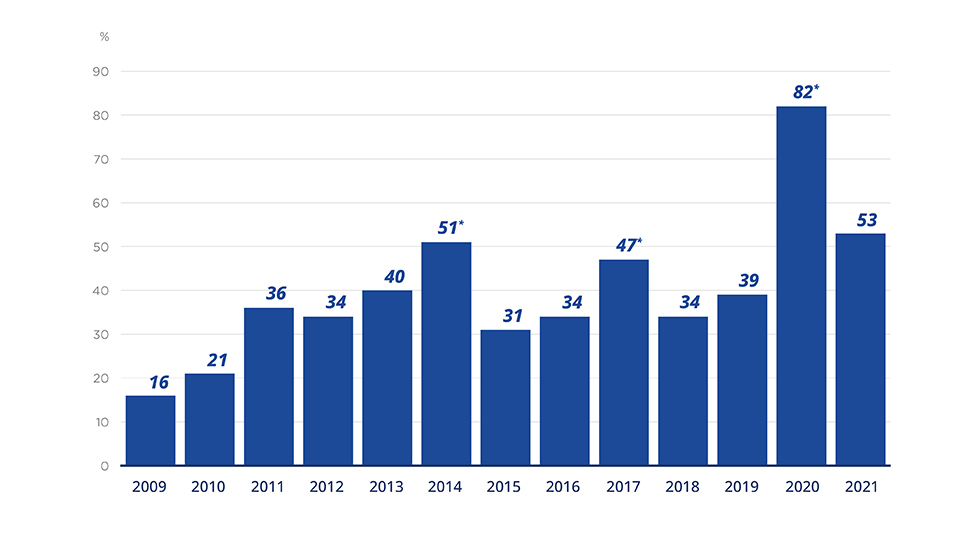

Source: SME Research Statistics Canada

This mechanism democratizes access to capital. Small businesses that might be rejected by traditional banks due to thin credit files can now secure funding based on their operational strength. As the industry evolves, the ability to process and interpret this alternative data becomes the primary differentiator between platforms, making AI underwriting the standard for fast, accessible SME credit 2026 solutions.

Best digital lending platforms for 2026

The landscape of SME credit 2026 has shifted decisively toward platforms that blend speed with sophisticated underwriting. Traditional banks are no longer the only gatekeepers; specialized fintech lenders now offer approval times measured in hours rather than weeks, powered by AI that analyzes cash flow data in real time.

For small business owners, this means access to working capital and growth funding is faster and more transparent. The following platforms represent the current leaders in this space, chosen for their proven track records, AI-driven efficiency, and ability to serve diverse SME needs.

HES LoanBox

HES LoanBox stands out for its modular architecture, allowing lenders to customize workflows quickly. It is particularly strong in automated document verification and risk assessment, making it a top choice for institutions looking to scale their SME lending operations without compromising on compliance.

Mambu

Mambu offers a cloud-native core banking system that supports high-volume lending. Its API-first approach allows seamless integration with third-party data providers, enabling dynamic credit scoring. This platform is ideal for lenders who need to process a large number of SME applications simultaneously with minimal manual intervention.

QUALCO Loan Manager

QUALCO Loan Manager focuses on simplicity and speed for mid-sized lenders. Its intuitive interface reduces the time spent on administrative tasks, allowing loan officers to focus on relationship building. The platform’s AI tools help identify high-potential SME borrowers by analyzing historical repayment patterns and current financial health.

American Express Business Blueprint

American Express Business Blueprint leverages the card issuer’s vast transaction data to offer tailored credit lines. This platform excels in providing credit to businesses with strong Amex usage history, often offering higher limits and lower rates based on actual spending behavior rather than just credit scores.

| Platform | Primary Strength | Best For |

|---|---|---|

| HES LoanBox | Customizable AI Workflows | Scaling Lenders |

| Mambu | Cloud-Native Scalability | High-Volume Operations |

| QUALCO Loan Manager | User-Friendly Interface | Mid-Sized Lenders |

| Amex Business Blueprint | Transaction-Based Underwriting | Existing Amex Merchants |

RWA-backed stablecoin credit options

Real-world asset (RWA) backed stablecoin lines of credit represent a niche but rapidly evolving segment of SME credit 2026. By tokenizing tangible assets like invoices, inventory, or real estate, platforms can issue stablecoins that settle instantly on-chain. This model offers tech-forward small businesses a high-efficiency alternative to traditional bank loans, which often struggle with sluggish processing times and rigid collateral requirements.

The primary appeal lies in speed and accessibility. While traditional lenders rely on credit scores and lengthy underwriting, RWA platforms can leverage on-chain data and asset verification to approve credit lines in hours rather than weeks. For SMEs that need immediate working capital to bridge cash flow gaps, this immediacy is transformative. However, borrowers must manage the technical landscape of digital wallets and smart contract interactions, which adds a layer of complexity not present in conventional banking.

Several emerging fintechs are positioning themselves at this intersection. These platforms typically partner with regulated custodians to hold the underlying real-world assets while issuing the corresponding stablecoin liquidity. This structure aims to provide the liquidity benefits of cryptocurrency with the stability of fiat-pegged tokens. As regulatory frameworks clarify, this sector is expected to attract more institutional capital, further lowering borrowing costs for qualified SMEs.

Checklist for choosing an SME lender

Securing SME credit 2026 requires more than a good business plan; you need a partner who understands your specific cash flow cycles. The right lender aligns with your growth stage, while the wrong one can drain resources through hidden fees or rigid terms. Use this step-by-step checklist to evaluate potential AI lending platforms before signing any agreements.

Modern AI platforms assess risk using real-time data rather than just historical credit scores. Ensure the lender explains how their algorithm calculates your rate. You need to know which data points—like bank statements or social media activity—influence your eligibility to avoid unexpected rejections.

Look beyond the headline interest rate. AI lenders often charge origination fees, processing costs, or early repayment penalties. Calculate the Annual Percentage Rate (APR) to see the true cost. A slightly higher rate with no hidden fees is often cheaper than a low-rate loan with steep administrative costs.

One advantage of AI lending is speed. Some platforms approve and fund loans within 24 hours, while traditional banks may take weeks. Determine if the platform offers flexible drawdown options, allowing you to borrow only what you need when you need it, rather than a lump sum that accrues interest immediately.

AI algorithms handle the paperwork, but humans should handle the problems. Check if the lender provides dedicated account managers or 24/7 support. If your application encounters a glitch or you need to restructure a payment, you need a responsive team, not just a chatbot, to resolve the issue quickly.

Top platforms often bundle lending with accounting software, invoicing, or cash flow forecasting tools. These integrations can simplify your financial management and provide the lender with better data, potentially improving your future borrowing terms. Prioritize lenders that offer value beyond just the loan itself.

Frequently asked questions about SME credit 2026

As the landscape for SME credit 2026 evolves, understanding the specific mechanics of financing and support is essential. Below are answers to the most common questions regarding eligibility, definitions, and government support programs.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!