Why SME credit is shifting in 2026

Traditional bank lending is stagnating. While new lending to SMEs has begun to recover slightly, the overall stock of SME loans remains broadly stagnant across many developed economies. This sluggish growth in institutional credit has created a significant capital gap for small businesses that cannot afford to wait months for a bank decision.

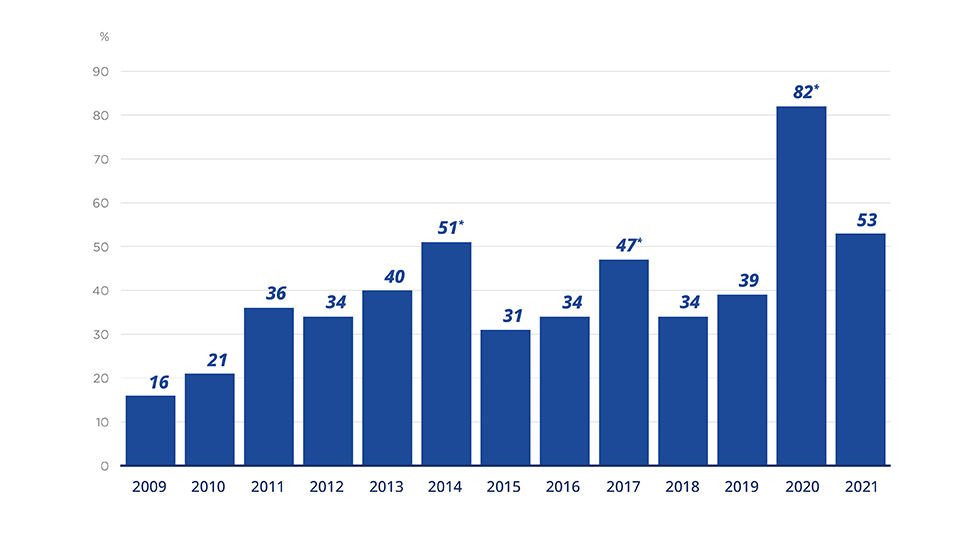

OECD data shows that the aggregate of SME long-term loan volumes has fallen by 11% in real terms over the recent period. This decline is not just a statistical blip; it represents a structural shift away from relationship-based banking toward more efficient, data-driven alternatives. Small and medium enterprises are increasingly turning to AI underwriting solutions that can process cash flow data, transaction history, and digital footprints in minutes rather than weeks.

Fintech platforms are filling this void by offering faster, data-rich underwriting processes. These tools do not replace human judgment entirely but augment it with real-time analytics that banks often lack. For SMEs, this means access to working capital when they need it most, based on actual business performance rather than just historical collateral. The result is a more dynamic credit market where speed and data accuracy are becoming the primary competitive advantages.

How AI underwriting changes approval odds

Legacy credit models often reject small businesses because they rely heavily on static metrics like credit scores and years in operation. This approach misses the real-time health of a company, leaving many viable borrowers in the "credit invisible" category. AI underwriting changes this by analyzing alternative data points, such as cash flow patterns, transaction history, and even supply chain stability, to build a dynamic risk profile.

By looking at how money moves rather than just what is on a balance sheet, lenders can approve borrowers who might otherwise be turned away. This shift allows for a more accurate assessment of repayment capacity, reducing the friction for SMEs seeking financing for operating expenses or expansion.

The result is a more inclusive lending landscape. Where traditional models see risk, AI-driven systems see nuance, allowing lenders to offer terms that reflect the actual performance of the business. This mechanism is becoming a standard expectation for SMEs in 2026, as the gap between traditional and alternative underwriting widens.

Top fintech lending platforms for SMEs

Selecting the right AI-driven lending platform requires matching specific business metrics to the underwriting engine’s data sources. While traditional banks rely heavily on FICO scores and historical financial statements, leading fintechs now ingest real-time cash flow, payroll data, and transaction history to approve loans in hours rather than weeks.

The platforms below represent the current market leaders in AI underwriting. They prioritize speed and accessibility for SMEs that may not meet conventional bank criteria, using alternative data to assess creditworthiness.

Kabbage

Kabbage (now part of American Express) remains a staple for small businesses seeking flexible lines of credit. Its AI engine connects directly to business accounts—including Amazon, Shopify, QuickBooks, and PayPal—to evaluate cash flow. This direct integration allows Kabbage to offer revolving credit limits that adjust based on real-time performance, making it ideal for businesses with seasonal revenue fluctuations.

OnDeck

OnDeck focuses on term loans and lines of credit for established small businesses. Its underwriting model incorporates non-traditional data points, such as business tenure and industry performance, to provide faster decisions than brick-and-mortar lenders. OnDeck is particularly effective for SMEs that have been in operation long enough to build a digital footprint but lack the extensive collateral required by traditional banks.

BlueVine

BlueVine specializes in no-fee lines of credit and invoice factoring. Its AI-driven approval process is designed for speed, often providing decisions within 24 hours. BlueVine’s platform allows businesses to draw funds as needed and pay interest only on the amount used, offering significant flexibility for working capital management without the burden of long-term debt.

Funding Circle

Funding Circle connects small businesses with a network of institutional investors, using AI to match borrowers with the most suitable loan terms. The platform assesses risk by analyzing a wide range of business data points, allowing it to offer competitive rates to creditworthy SMEs. Funding Circle is particularly useful for businesses seeking larger term loans for expansion or equipment purchases.

Lendio

Lendio acts as a marketplace rather than a direct lender, using AI to match SMEs with a network of over 100 lending partners. This approach increases the likelihood of approval by presenting the borrower’s profile to multiple lenders simultaneously. Lendio’s platform is best suited for businesses that want to explore a variety of loan products, from SBA loans to term loans, without submitting to multiple hard credit checks.

| Platform | Primary Product | Approval Speed | AI Data Focus |

|---|---|---|---|

| Kabbage | Revolving Credit Line | Minutes to 24 Hours | Real-time Cash Flow & Transactions |

| OnDeck | Term Loans & Lines of Credit | 24 to 48 Hours | Business Tenure & Industry Data |

| BlueVine | No-Fee Lines of Credit | 24 Hours | Bank & Payroll Data |

| Funding Circle | Term Loans | 1 to 3 Days | Comprehensive Business Metrics |

| Lendio | Marketplace Matching | Varies by Lender | Broad Lender Network Matching |

As an Amazon Associate, we may earn from qualifying purchases.

Choosing the right credit line for your business

AI underwriting has expanded the universe of available capital, but not every solution fits every cash flow pattern. The gap between traditional bank loans and modern fintech lines of credit often comes down to speed versus cost. You need to match the tool to the specific rhythm of your revenue.

Evaluate your cash flow cycle

If your revenue is seasonal or irregular, a traditional term loan might create repayment friction. Instead, look for AI-driven lines of credit that adjust limits based on real-time sales data. These tools analyze transaction history to offer flexibility that static models cannot. For example, a retailer stocking for the holidays benefits from a credit line that expands during peak months and contracts during slow periods.

Assess the total cost of capital

AI models often approve faster loans with higher fees to offset the speed of decision-making. While a 30-second approval is tempting, the annual percentage rate (APR) can significantly impact your bottom line. Compare the effective cost of a merchant cash advance against a term loan. Use the data to determine if the speed premium is worth the extra expense for your current liquidity needs.

Review the integration requirements

Seamless integration with your existing accounting software is non-negotiable. AI underwriting relies on accurate, up-to-date data. If a lender requires manual uploads or complex API setups, the administrative burden may outweigh the benefits. Prioritize solutions that sync automatically with platforms like QuickBooks or Xero to ensure the AI model has the freshest data for accurate risk assessment.

Common questions about SME credit in 2026

As AI-driven underwriting reshapes the lending landscape, small business owners face new questions regarding transparency and eligibility. Understanding how algorithms assess risk helps you prepare the right documentation and choose the right lender.

No comments yet. Be the first to share your thoughts!