2026 SME credit landscape

The macroeconomic environment for small and medium enterprises in 2026 is defined by a sharp divergence between traditional banking caution and the rapid expansion of alternative capital sources. While global economic activity has stabilized, the cost of debt remains elevated, forcing a structural shift in how SMEs access funding. Traditional lenders have tightened their criteria significantly, creating a financing gap that non-bank providers and digital platforms are actively filling.

According to the OECD, the aggregate volume of SME long-term loans has fallen by 11% in real terms over the past year [src-serp-1]. This contraction reflects a broader risk-aversion among commercial banks, which are prioritizing balance sheet stability over market share growth in a high-interest-rate regime. The result is a credit squeeze for businesses that do not fit the narrow profiles preferred by legacy institutions.

This tightening is not uniform. While traditional term loans are shrinking, alternative financing channels—including revenue-based financing, invoice discounting, and AI-driven underwriting platforms—have seen increased adoption. The Federal Reserve’s 2026 Main Street Metrics indicate that while access to credit has become more difficult, demand for flexible, short-term working capital solutions has surged among small businesses seeking to manage cash flow volatility [src-serp-6].

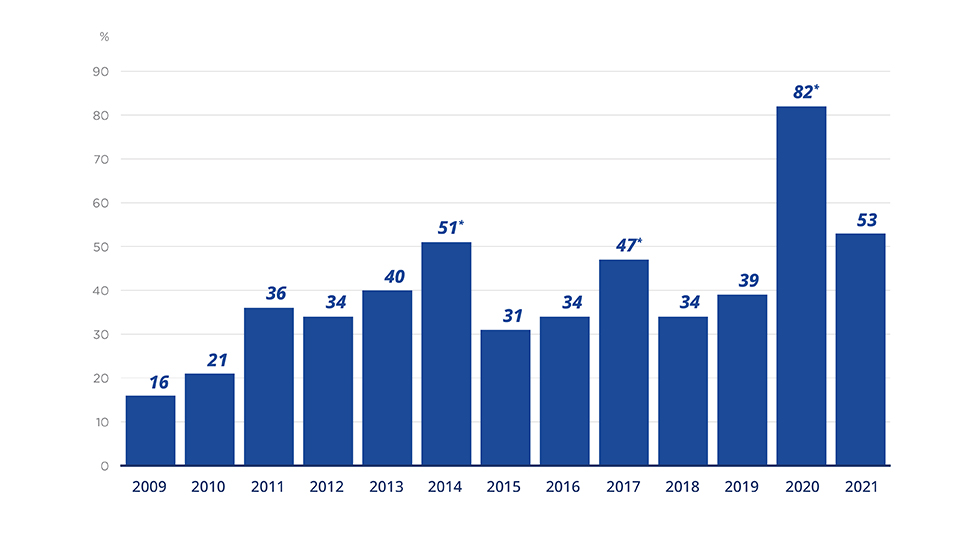

To visualize the broader credit environment, the following chart illustrates recent trends in SME credit indices, highlighting the divergence between traditional loan volumes and emerging alternative credit metrics.

The landscape is no longer binary. SMEs are increasingly expected to maintain a diversified funding stack, blending traditional relationships with digital-first lenders. This shift is driven by necessity as much as innovation, as businesses seek to mitigate the risks associated with relying on a single, tightening source of capital.

AI scoring replaces traditional credit checks

Traditional credit checks rely heavily on historical data that often fails to capture the current reality of a small business. For many SMEs, especially those with thin credit files or rapid growth, a static credit score is an incomplete picture. In 2026, AI-driven alternative credit scoring is shifting this paradigm by analyzing real-time cash flow, transaction history, and operational data. This shift directly addresses the need for fast approval business loans, allowing lenders to assess risk with greater precision and speed.

By processing vast amounts of unstructured data, AI models can identify patterns that traditional algorithms miss. A business might have a moderate credit score but demonstrate strong, consistent revenue streams and low volatility. AI scoring captures this nuance, enabling lenders to approve loans in minutes rather than weeks. This speed is critical for SMEs that need capital to seize immediate opportunities or manage short-term cash flow gaps.

The result is a more inclusive lending environment. Businesses that were previously excluded from traditional financing channels now have access to capital based on their actual performance rather than just their credit history. This shift not only accelerates funding but also reduces the cost of capital for well-managed SMEs, as lenders can price risk more accurately.

RWA stablecoins offer new credit lines

Real World Asset (RWA) stablecoins are emerging as a distinct asset class within the broader digital currency ecosystem, primarily serving as a bridge between traditional finance and blockchain liquidity. Unlike algorithmic stablecoins or those backed solely by volatile cryptocurrencies, RWA tokens are collateralized by tangible assets such as treasury bills, corporate bonds, or real estate. This structure allows small and medium enterprises (SMEs) to access credit lines without diluting equity or navigating the lengthy approval processes of traditional banking.

The mechanism is straightforward: an SME pledges tokenized assets as collateral to mint a stablecoin, which can then be used for operational liquidity. This process mirrors traditional secured lending but operates on a permissioned blockchain, offering faster settlement times and 24/7 availability. According to recent market analyses, private credit is entering 2026 in a challenging environment, making alternative liquidity sources increasingly attractive to businesses that may not qualify for conventional bank loans [src-serp-5].

The following comparison highlights the structural differences between traditional SME loans and RWA-backed stablecoin lines:

| Feature | Traditional SME Loan | RWA Stablecoin Line |

|---|---|---|

| Approval Speed | 2–8 weeks | Minutes to days |

| Collateral Type | Physical assets, personal guarantees | Tokenized treasuries, bonds |

| Interest Rate | Fixed or variable, bank-dependent | Dynamic, yield-based |

| Liquidity Access | Restricted, prepayment penalties | On-demand, programmable |

This model reduces the friction of capital access. By tokenizing existing assets, SMEs can unlock trapped value. The OECD has noted that digital asset integration is reshaping credit availability, particularly for firms with strong balance sheets but limited banking relationships [src-1]. As regulatory frameworks mature, RWA stablecoins are likely to become a standard tool for corporate treasury management, offering a transparent and efficient alternative to traditional debt instruments.

Choosing the right financing strategy

Selecting the correct credit facility requires matching the instrument to your cash flow cycle and risk tolerance. As capital markets shift in 2026, the gap between traditional bank lending and alternative financing continues to widen. Moody’s and OECD data suggest that SMEs relying solely on legacy bank loans may face tighter underwriting standards, while those adopting AI-driven or blockchain-based credit lines must navigate distinct operational risks.

The following framework helps you evaluate which financing path aligns with your immediate liquidity needs and long-term stability.

Traditional bank loans remain the lowest-cost option for established SMEs with strong balance sheets. However, approval cycles are slow, and collateral requirements are stringent. Evaluate your current debt-to-income ratio and collateral liquidity before applying. This path suits businesses with predictable, long-term cash flows that do not require rapid capital deployment.

Fintech lenders use alternative data and machine learning to approve loans in days rather than months. Interest rates are typically higher than banks, but the speed and flexibility support working capital needs. This option is ideal for SMEs with limited collateral but strong digital transaction histories. Ensure your accounting data is clean and accessible for automated underwriting.

Real-world asset (RWA) stablecoins offer programmable credit lines secured by tokenized assets. This emerging sector provides near-instant settlement and lower intermediary fees, but introduces smart contract and regulatory risks. Use this only if your team has technical expertise in digital asset management and your business can withstand volatility in collateral valuation.

Before committing to any financing strategy, verify the lender’s regulatory standing and fee structure. A mismatch between your cash flow timing and repayment terms can destabilize operations faster than high interest rates. Prioritize transparency and flexibility when evaluating new credit products in this evolving landscape.

No comments yet. Be the first to share your thoughts!