The 2026 SME credit landscape

Small and medium enterprises (SMEs) face a persistent liquidity constraint that limits their ability to invest in growth. According to the World Bank, SMEs face a $5.7 trillion finance gap across 119 emerging market and developing economies. This shortfall creates a bottleneck that traditional banking models have struggled to resolve for decades.

The friction stems from how lenders assess risk. Traditional banks often rely on historical financial statements and physical collateral, which many fast-growing or digital-first SMEs lack. As a result, many viable businesses are either denied credit or forced to accept terms that stifle expansion. The OECD notes that sluggish growth in SME credit is directly weighing on firm liquidity and competitiveness, particularly in regions where digital infrastructure is still maturing.

2026 marks a shift in this dynamic. New lending models are beginning to bridge the gap by leveraging real-time data and tokenized assets. Instead of relying solely on static balance sheets, lenders are using AI to analyze cash flow patterns, transaction history, and even supply chain data to underwrite loans. Simultaneously, the rise of Real World Asset (RWA) tokenization allows SMEs to use physical assets or future receivables as collateral, unlocking liquidity that was previously locked away.

This transition is not just about technology; it is about accessibility. For business owners, this means faster approval times and more flexible credit lines. For the broader economy, it represents an opportunity to unlock trillions in dormant capital. As these tools become mainstream, the SME credit landscape is moving from a system of exclusion to one of inclusion, powered by data and digital trust.

AI models for alternative credit scoring

Traditional FICO scores are no longer the only gatekeeper for SME lending. In 2026, lenders are increasingly relying on AI models that analyze a business’s digital footprint and real-time data health to assess creditworthiness. This shift allows lenders to look beyond static financial statements and capture the dynamic reality of small businesses that may have thin credit files but strong operational momentum.

These AI-driven systems process vast amounts of alternative data points, such as cash flow patterns from accounting software, transaction histories from payment processors, and even behavioral signals from e-commerce platforms. By integrating these diverse data streams, lenders can construct a more nuanced profile of a borrower’s ability to repay. This approach significantly reduces the friction for early-stage companies or those with limited credit history, enabling faster approval times and more personalized lending terms.

The move toward alternative scoring is particularly impactful for "thin-file" SMEs. Instead of being rejected due to a lack of traditional credit history, these businesses can now demonstrate their viability through their digital activity. Lenders use machine learning algorithms to identify patterns that correlate with successful loan repayment, effectively democratizing access to capital for entrepreneurs who were previously overlooked by traditional banking models.

As an Amazon Associate, we may earn from qualifying purchases.

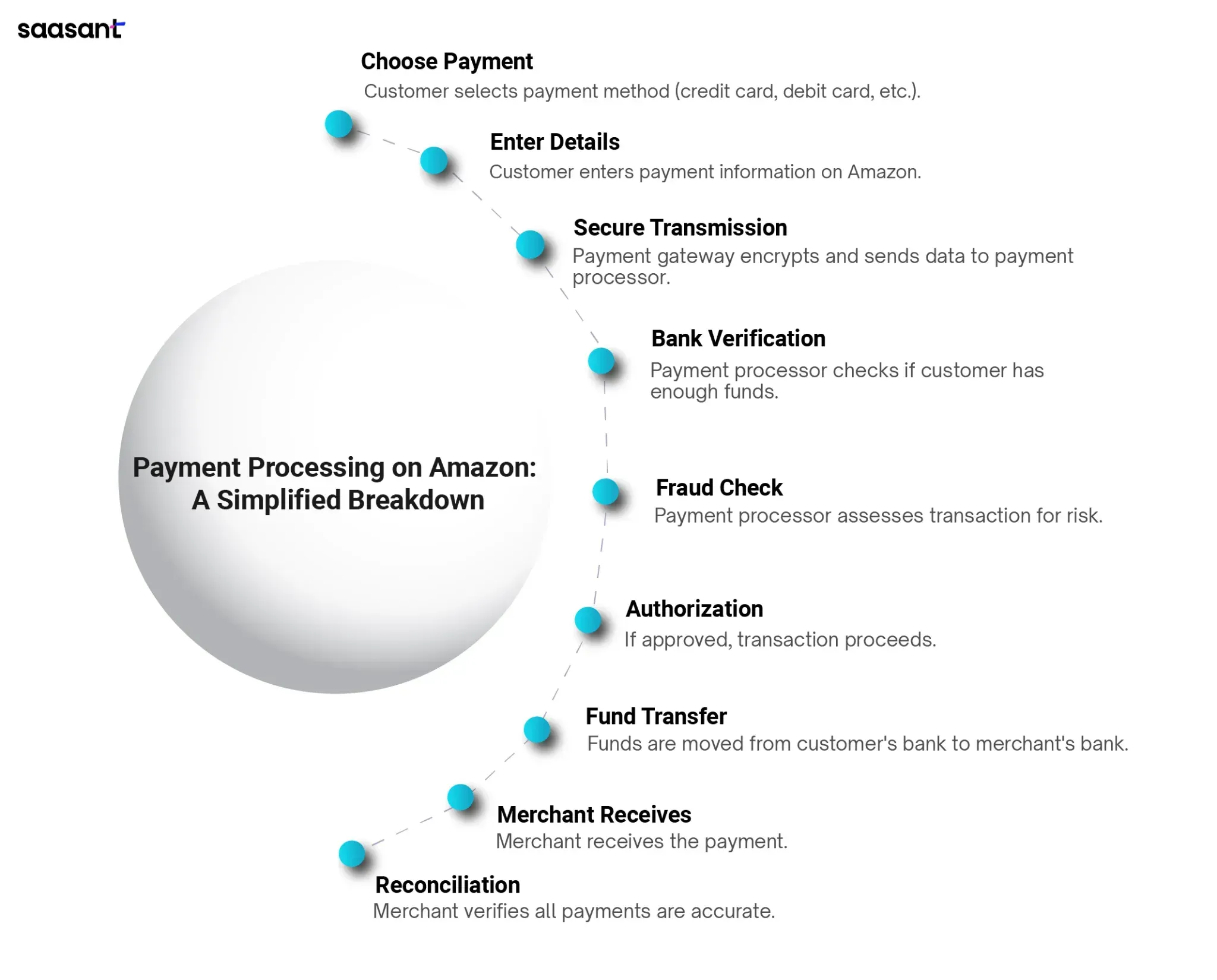

How RWA-backed stablecoin credit works

Real World Assets (RWA) allow businesses to lock up traditional collateral—such as treasury bills, invoices, or real estate—in a smart contract to unlock immediate stablecoin liquidity. Instead of waiting weeks for a bank underwriter to review physical documents and approve a loan, the protocol automatically verifies the asset's existence and value on-chain. Once the asset is tokenized and locked, the system issues a corresponding line of credit in USDC or another stablecoin.

This mechanism shifts the bottleneck from human processing speed to blockchain settlement time. Traditional SME loans often require days of administrative overhead. With RWA-backed lines, approval happens in minutes or hours, and funds are available 24/7, including weekends and holidays. This continuous availability is critical for businesses that need to cover payroll, purchase inventory, or manage cash flow gaps that don't align with standard banking business hours.

The collateral remains secure and auditable. Because the underlying assets are verified by trusted oracles or custodians, lenders can offer competitive interest rates that are often lower than unsecured digital loans. The borrower retains ownership of the underlying asset while using the stablecoin for operations, repaying the loan by unlocking the collateral when the debt is settled.

For businesses exploring these financing tools, having the right operational infrastructure is essential. Just as a physical store needs reliable shelving to display goods, a digital-first business needs robust tools to manage its new digital assets. The following products represent popular tools and accessories that SMEs often use to support their digital finance and operational workflows.

As an Amazon Associate, we may earn from qualifying purchases.

Software and instruments for managing SME cash flow

SME credit is no longer just about securing a loan; it is about maintaining liquidity in a market where time and certainty are scarce. The OECD notes that sluggish growth in traditional SME credit is weighing heavily on firm liquidity, making real-time visibility essential. To bridge the gap between slow banking cycles and immediate operational needs, businesses are turning to a mix of specialized software and alternative financial instruments.

Cash flow monitoring tools

Visibility is the first step in managing liquidity. Platforms like Float and Pulse integrate with accounting software to project cash positions weeks or months in advance. These tools do not just report history; they forecast shortfalls before they disrupt payroll or supplier payments. By visualizing the runway, owners can make proactive decisions about drawdowns on credit lines rather than reacting to crises.

RWA-backed lines of credit

For immediate capital, Real World Asset-backed lines of credit are emerging as a faster alternative to traditional bank loans. These instruments use tokenized assets as collateral to unlock liquidity, often processing approvals in days rather than months. This approach decouples credit access from rigid banking cycles, allowing SMEs to tap into capital when opportunities arise.

Comparing lending options

The shift toward AI-driven and RWA-backed lending changes the cost-benefit analysis for SMEs. While traditional banks offer lower interest rates, the speed and accessibility of alternative credit lines often justify the higher cost for urgent working capital needs.

| Feature | Traditional Bank Line | AI/RWA-Backed Line |

|---|---|---|

| Approval Speed | 2-6 weeks | 24-72 hours |

| Collateral Requirement | Heavy personal/business assets | Tokenized RWA or receivables |

| Cost of Capital | Lower interest rates | Higher but predictable fees |

| Accessibility | Strict credit score thresholds | Data-driven underwriting |

Product recommendations

Selecting the right tool depends on whether you need visibility, immediate capital, or both. The following products represent leading solutions in cash flow forecasting and alternative credit access.

As an Amazon Associate, we may earn from qualifying purchases.

Build business credit in 2026

Establishing a credit profile requires treating your business as a distinct legal and financial entity. Start by forming a corporation or LLC and securing your EIN and D-U-N-S number. Open a dedicated business bank account to separate personal and commercial transactions. This separation is the foundation for any creditworthiness assessment.

Next, establish trade lines with vendors that report to business credit bureaus. These accounts function like credit cards but are often easier to qualify for. Use them for regular purchases and pay the balance in full each month. Consistent on-time payments build your payment history, which is the primary driver of your business credit score.

Once your profile is active, apply for a business credit card or a line of credit. Choose products that report to all three major business credit bureaus. To support your application with tangible assets, consider securing inventory or equipment that can serve as collateral or operational proof.

As an Amazon Associate, we may earn from qualifying purchases.

Frequently asked questions about SME credit

Understanding the nuances of business financing can be the difference between smooth operations and cash flow bottlenecks. Below are answers to the most common questions regarding SME credit, subsidies, and lender selection.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!