Why SME credit 2026 needs new tools

Traditional banking is tightening its grip on small businesses. Lower interest rates alone have not restored growth; credit terms remain restrictive and long-term borrowing is weakening for SMEs. This shift leaves many companies unable to secure the working capital they need to operate.

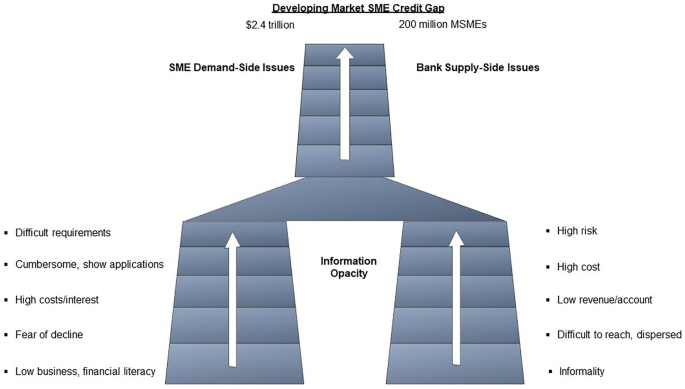

The challenge is global. According to the World Bank, small and medium enterprises face a $5.7 trillion finance gap across emerging markets and developing economies. This shortage stifles innovation and limits job creation, particularly for women-led businesses. SMEs power economies, yet they are often priced out or locked out of traditional lending channels.

RWA-backed stablecoins offer a faster, data-driven alternative. By tokenizing real-world assets, lenders can access real-time transaction data rather than relying solely on historical credit scores. This approach reduces friction and opens up liquidity to businesses that traditional banks deem too risky.

Compare lending platforms and terms

When evaluating RWA-backed lending platforms for SME credit, the differences in cost and speed matter most. Traditional banks often require weeks for approval and charge higher rates due to overhead. Stablecoin lines, by contrast, offer near-instant liquidity with transparent, algorithmic pricing.

Use a comparison table to weigh APRs, collateral ratios, and funding times. This helps you identify which platform fits your cash flow needs without getting lost in marketing jargon.

| Platform | APR Range | Collateral Type | Approval Time |

|---|---|---|---|

| HES LoanBox | 6-12% | USDC/USDT | < 1 hour |

| Mambu | 8-15% | Crypto + RWA | 1-3 days |

| Kredo | 5-10% | Real Estate RWA | 2-5 days |

| Tradeplus24 | 7-14% | Receivables | 24-48 hours |

The image below shows a typical SME credit facility overview. While this example is from a traditional bank, the same due diligence applies to digital platforms: read the fine print on collateral liquidation triggers.

Prepare your business data for AI scoring

Traditional underwriting relies on static snapshots: annual tax returns and quarterly balance sheets. AI-driven stablecoin credit lines require a different feed. Lenders need real-time visibility into cash flow velocity and operational stability to price risk accurately. Your goal is to transform fragmented financial records into a clean, verifiable data stream.

Start by consolidating your transaction history. AI models analyze patterns in payment timing, vendor reliability, and customer churn. Ensure your accounting software exports data in a standard format like CSV or JSON. Remove duplicate entries and categorize expenses consistently. Inconsistent data introduces noise that degrades the credit score.

Next, integrate your primary bank statements and payment processor logs. Stablecoin lenders often cross-reference on-chain activity with fiat inflows to verify business legitimacy. Link your business checking account via a secure aggregator. This provides the "real-time" stability metrics that static PDFs cannot offer.

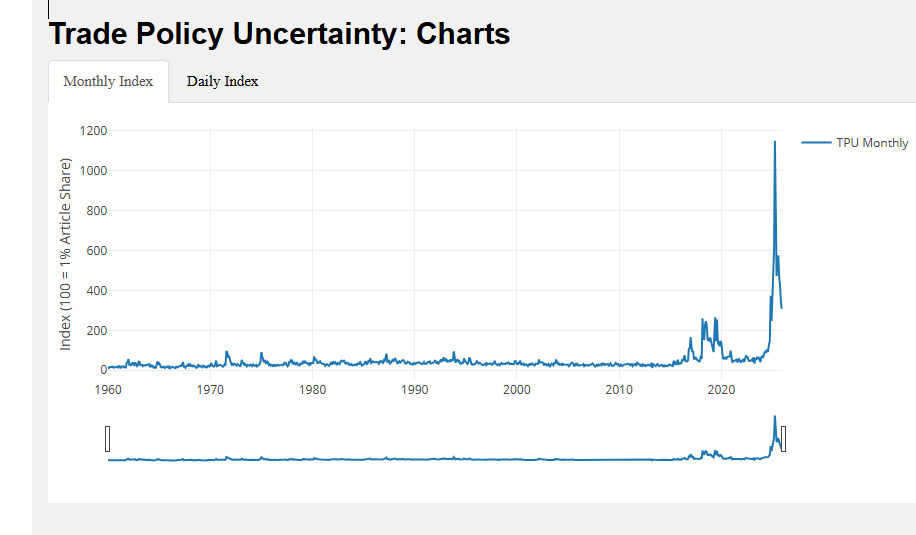

Finally, prepare your supply chain documentation. Recent trade policy uncertainty has made supply chain resilience a key risk factor for SMEs. Gather contracts with key suppliers and log any recent delays or cost increases. This context helps the AI distinguish between temporary cash flow dips and structural business weaknesses.

Export 12–24 months of transaction data from your accounting platform. Remove duplicates, standardize categories, and ensure all recurring payments are clearly tagged. Clean data is the foundation of accurate AI scoring.

Connect your primary business bank account and payment gateways (Stripe, Square, etc.) using a secure API aggregator. This allows lenders to verify real-time cash flow and cross-reference fiat activity with on-chain transactions.

Gather active contracts with top suppliers and log any recent delays or cost fluctuations. This data helps the underwriting AI assess operational stability and resilience against trade policy shifts.

Execute the stablecoin credit application

Applying for an SME credit line using stablecoins follows a structured workflow. You move from account verification to collateral deposit, and finally to credit line activation. The process is designed to be automated, reducing the manual underwriting delays typical of traditional bank loans.

The primary keyword focus here is on the execution of the stablecoin credit application. This section details the exact steps required to secure your funding.

Start by completing Know Your Business (KYB) checks. Lending platforms require proof of incorporation, beneficial ownership details, and tax identification numbers. This step ensures regulatory compliance before any financial transactions occur. Most platforms complete this verification within 24 hours if documents are submitted correctly.

Once approved, deposit your chosen collateral into the platform’s smart contract. Common assets include USDC, USDT, or wrapped Ethereum. The system calculates the loan-to-value (LTV) ratio in real time. For example, a 50% LTV means you must deposit $10,000 in stablecoins to access a $5,000 credit line. Ensure your wallet has sufficient gas fees for the transaction.

After collateral is locked, the credit line becomes active. You can draw funds as needed, often with instant settlement. Interest typically accrues only on the amount drawn, not the total limit. Repayments can be made at any time without prepayment penalties, allowing you to manage cash flow efficiently. Monitor your health factor to avoid liquidation if collateral value drops.

Common mistakes in digital lending

Even with stablecoin infrastructure, SME credit applications fail when founders treat smart contracts like traditional bank forms. The code executes exactly what it is told, not what you intended. One misplaced variable in a collateral ratio can liquidate your entire position before you realize the error.

The most frequent error is over-collateralization. Lenders require a safety buffer—often 150% to 200% of the loan value—to absorb volatility. Founders often miscalculate this by ignoring the stablecoin’s peg risk or their own asset’s liquidity. If your collateral asset drops in value, the protocol may trigger a margin call instantly. Unlike a bank manager who might give you a grace period, a smart contract has no discretion. It sells your assets at the worst possible market price.

Another pitfall is ignoring the smart contract’s upgradeability. Many DeFi lending protocols allow developers to modify the core logic via multi-sig wallets. If the governance team is compromised or makes a bad upgrade, your funds are at risk. Always check the contract’s audit history and the time-lock period for upgrades. Never deposit funds into a protocol with a history of unverified changes.

Finally, don’t underestimate gas fees. On congested networks, transaction costs can eat up a significant portion of a small loan. Calculate the net benefit of the credit line against the cost of borrowing and transacting. If the fees outweigh the interest savings, the deal is not viable.

Check your eligibility and next steps

Before submitting your application for an SME credit line, ensure your documentation is audit-ready. Lenders reviewing stablecoin-backed facilities require the same rigor as traditional banks, plus proof of digital asset compliance.

Pre-application checklist

-

KYC/AML Verification: Ensure all beneficial owners are verified with government-issued IDs. Stablecoin lenders often require stricter source-of-funds documentation.

-

Bank Statements: Provide 6-12 months of business bank statements. Lenders use these to verify cash flow stability against debt service requirements.

-

Collateral Liquidity: Confirm your stablecoin holdings are in a compatible wallet or exchange account that supports instant liquidity for margin calls.

-

Credit History: Check your personal and business credit scores. While on-chain history matters, traditional credit still influences interest rates.

Next steps for approval

Once your documents are organized, submit your application through the lender’s portal. Expect a 24-48 hour review period for initial eligibility. If approved, you will receive a digital loan agreement. Sign it electronically and fund your collateral wallet to activate your credit line.

No comments yet. Be the first to share your thoughts!