Get sme credit trends 2026 right

Before you apply for financing, understand that 2026 is a year of tighter credit and faster decisions. OECD data shows a significant drop in long-term loan volumes, meaning banks are becoming more selective. At the same time, AI-driven underwriting is changing how lenders assess risk, favoring digital readiness over traditional collateral.

To succeed, you need to prepare two things: clean financial data and a clear narrative. Lenders now use automated systems that scan your digital footprint. If your books are messy or your cash flow is unpredictable, the algorithm will reject you before a human ever sees the application.

Start by organizing your last 24 months of bank statements and tax returns. Ensure your invoicing system is up to date and accessible. Lenders want to see consistent revenue, not spikes. If you have pending invoices, list them clearly. This transparency helps the AI model trust your income stability.

Also, check your credit score and business registration details. Small errors here can cause automatic rejections. Take the time to verify everything before you submit. Being prepared now saves weeks of back-and-forth later.

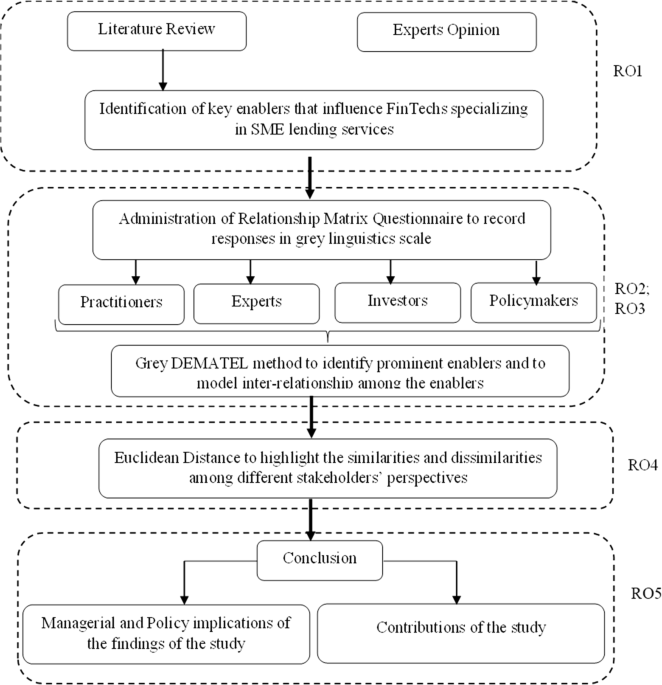

Work through the steps

SME Credit Trends works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

Common Mistakes in AI-Driven SME Lending

AI-driven underwriting promises speed, but it often introduces new blind spots that can hurt small business owners. The most frequent errors stem from over-reliance on automated signals while ignoring the nuanced reality of cash flow and operational stability. Understanding these pitfalls helps lenders refine their models and borrowers prepare stronger applications.

Ignoring Cash Flow Volatility

Many AI models prioritize static financial ratios or historical credit scores, failing to account for the seasonal or irregular nature of small business revenue. A business might appear healthy based on last year’s tax returns but struggle with immediate liquidity due to a slow quarter. Lenders who do not integrate real-time transaction data or account for industry-specific cycles risk rejecting viable applicants or approving those facing imminent shortfalls.

Overweighting Digital Footprints

There is a growing trend to use alternative data—such as social media activity, website traffic, or email engagement—as proxy indicators for creditworthiness. While this can help thin-file borrowers, it often correlates more with marketing effort than repayment ability. A high-traffic e-commerce site does not guarantee profit margins. Relying too heavily on these digital signals can inflate approval rates for businesses that lack the underlying financial discipline to service debt.

Failing to Explain Denials

Regulatory frameworks and consumer trust demand transparency in lending decisions. However, many AI underwriting systems operate as black boxes, making it difficult to explain why a loan was denied. If a lender cannot clearly articulate which factor triggered a rejection—such as a specific debt-to-income ratio threshold or a drop in cash reserves—the borrower has no path to correction. This lack of explainability erodes trust and leaves small businesses stuck in a cycle of repeated, unexplained rejections.

Assuming Uniform Risk Across Sectors

AI models trained on broad economic data often fail to capture sector-specific risks. For instance, a model trained on retail trends may misinterpret the supply chain vulnerabilities of a manufacturing SME. Treating all small businesses with similar algorithmic weights ignores the distinct operational challenges of healthcare, construction, or hospitality. Lenders must adjust their AI parameters to reflect the unique risk profiles of different industries to avoid systemic bias.

Neglecting the Human Element

Finally, the most significant mistake is assuming AI can fully replace human judgment in complex cases. Automated systems excel at processing high volumes of standard applications, but they often miss contextual nuances. A sudden drop in revenue might be due to a temporary supply chain issue rather than poor management. Without a human review layer for edge cases, lenders may reject good borrowers based on algorithmic rigidity, missing opportunities for relationship-building and long-term loyalty.

Sme credit trends 2026: what to check next

Navigating 2026 lending requires understanding how AI underwriting changes approval odds and timelines. Here are practical answers to common concerns about accessing capital for small businesses.

No comments yet. Be the first to share your thoughts!