In the bustling landscape of 2026 finance, small and medium-sized enterprises (SMEs) face a familiar crunch: delayed payments from invoices tying up vital cash flow. Traditional banks often drag their feet with lengthy approvals and high fees, but RWA-backed stablecoin lines of credit are flipping the script. By tokenizing real-world assets like receivables, platforms now deliver instant liquidity through blockchain-powered stablecoin invoice financing for small businesses. As tokenized RWAs hit $24 billion by mid-2025, with private credit surging past $14 billion, this model promises yields of 8-12% for lenders while slashing costs for borrowers to as low as 12% annualized.

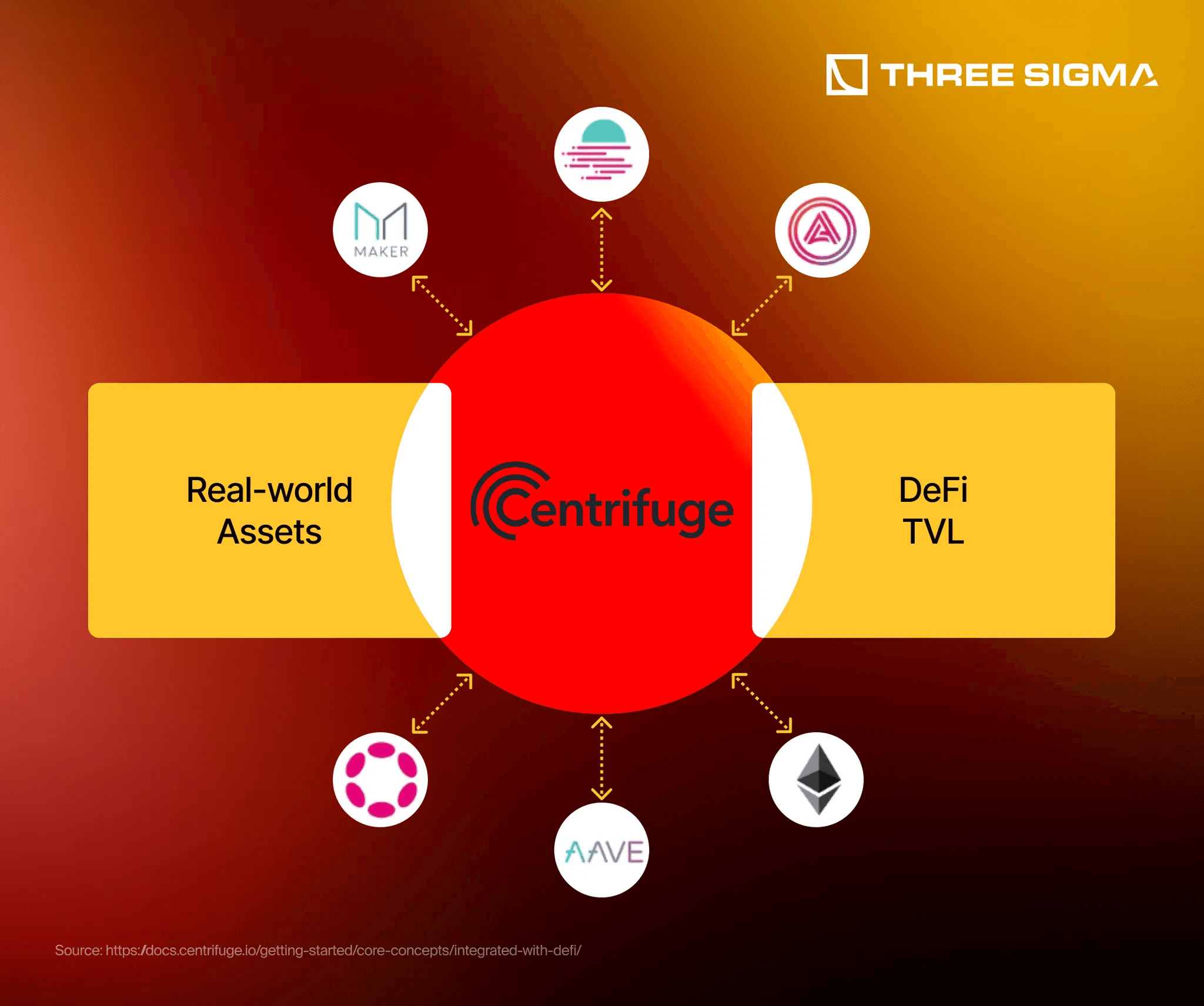

Centrifuge leads the charge here, tokenizing invoices and SME loans to unlock DeFi liquidity. Its focus on trade finance aligns perfectly with supply chain pressures in Asian markets, where I've seen hybrids like these thrive amid regulatory tailwinds. a16z crypto highlights how new protocols enable onchain lending against offchain collateral, a trend accelerating into 2026.

Tokenized Private Credit Fuels SME Growth

Private on-chain credit isn't hype; it's a trillion-dollar pivot from legacy debt markets. Maple Finance and Goldfinch exemplify this, channeling stablecoin capital into underbanked SMEs. Borrowers access RWA working capital lines of credit without selling assets outright, retaining upside while securing funds in hours, not weeks. McKinsey notes stablecoins reshaping payments, with 2025 tailwinds spilling into broader adoption. For SMEs, this means converting receivables into tradable tokens, bypassing factoring middlemen.

Key 2026 RWA Stablecoin Trends

- Tokenized Invoices: Platforms like Centrifuge and Maple Finance tokenize SME receivables, bridging real-world cash flows to DeFi for instant liquidity.

- Shariah-Compliant Models: SILQFi and Helix launched tokenized invoice financing in the Gulf, combining on-chain infrastructure with Islamic finance principles.

- Asian Regulatory Nods: HKMA to issue first stablecoin licenses by March 2026; South Korea's BDACS launches KRW1 on Plume network.

- DeFi Yields 8-12%: Tokenized private credit on Goldfinch and Maple Finance offers SME borrowers competitive yields amid $24B RWA market growth.

- Key Partnerships: Ozean and Nexade integrate $100M in SME invoice financing, linking DeFi with traditional capital access.

I've analyzed these protocols closely; their smart contracts automate compliance and risk assessment, reducing default rates through transparent oracles. Citigroup's 2030 outlook flags SME financing as a prime stablecoin use case, especially as deposit-backed intermediation wanes.

Partnerships Bridge TradFi and DeFi Worlds

Real momentum builds through collaborations. Ozean's November 2024 tie-up with Nexade injects up to $100 million in invoice opportunities onchain, targeting SMEs starved for capital. Similarly, SILQFi and Helix's August 2025 Shariah-compliant launch in the Gulf channels stablecoins into ethical financing, blending regional know-how with blockchain rails. These moves enhance financial inclusion, letting SMEs in emerging markets tap global liquidity pools.

Such alliances underscore a balanced evolution: DeFi's speed meets TradFi's diligence. In Asia, where I've spent 15 years navigating fintech, BDACS's KRW1 stablecoin on Plume signals Korea's RWA push, complementing HKMA's March 2026 licenses for structured issuance.

Stablecoin Backbone Enables Seamless LOCs

At the core, innovations like Ondo Finance's $USDY - backed by U. S. Treasuries and deposits - offer onchain stability with dividends. This underpins asset-backed stablecoin loans for SMEs, ensuring pegged value amid volatility. FinTech Weekly predicts regulation and institutional inflows will redefine stablecoin roles by 2026, powering blockchain SME credit at scale. Platforms like Centrifuge tokenize non-traditional assets, bridging cash flows to DeFi without intermediaries' drag.

Centrifuge's protocol, for instance, stands out in my analysis of Asian supply chains, where invoice delays average 60-90 days. By tokenizing these receivables, SMEs gain immediate access to stablecoin invoice financing for small businesses, with liquidity pools drawing institutional capital at competitive rates.

Navigating Implementation: A Practical Roadmap

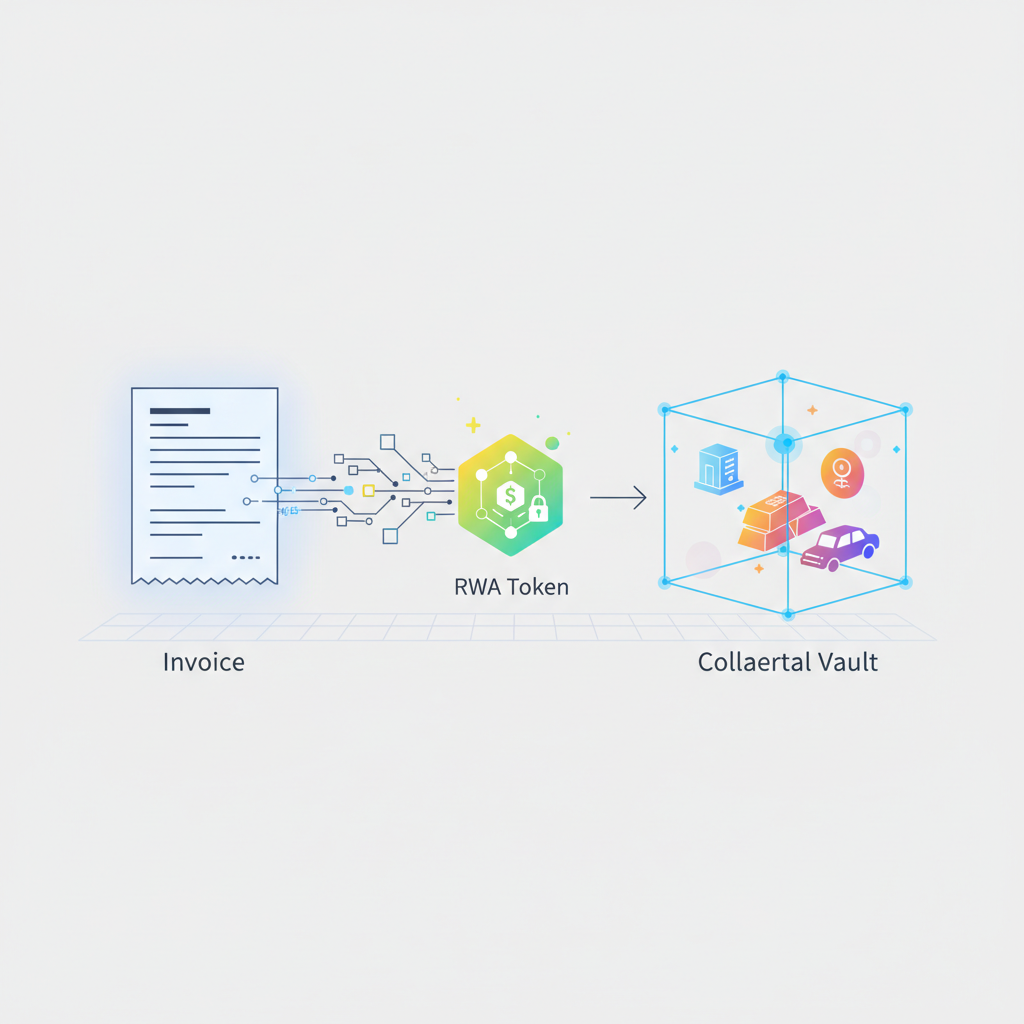

Securing an RWA-backed stablecoin line of credit starts with uploading verified invoices to a platform like those powered by Centrifuge or emerging hybrids. Smart contracts verify authenticity via oracles, collateralize the asset, and issue stablecoins against 70-90% of invoice value. Repayment triggers automatic token burn and asset release, all settled in under 24 hours. This efficiency, observed in pilots across Southeast Asia, cuts administrative overhead by 40% compared to banks.

Unlock Invoice Liquidity: 5-Step Guide to RWA-Backed Stablecoin LOCs for SMEs

From my vantage in hybrid fintech, the beauty lies in customization. SMEs can draw revolving credit, scale with business cycles, and even layer Shariah-compliant structures for Gulf operations. Ozean-Nexade's $100 million infusion exemplifies scalable impact, while HKMA's licenses will catalyze Asian adoption by formalizing issuer standards.

Risks and Mitigations in Blockchain SME Credit

No innovation skips pitfalls. Smart contract vulnerabilities demand audited code, as seen in past DeFi exploits, though platforms now integrate multi-sig and insurance layers. Oracle risks - mismatched offchain data - are tempered by diversified feeds. For SMEs, credit scoring via onchain history builds trust, but initial bootstrapping favors established firms. Yields of 8-12% reflect this; lenders price in illiquidity premiums, yet defaults hover below 2% in tokenized pools, per recent data.

Balanced against these, the upsides dominate. Cost savings hit 12% annualized versus 20% and traditional factoring, per industry benchmarks. Regulatory nods, from HKMA to Gulf initiatives, de-risk the space, positioning blockchain SME credit 2026 as a staple.

SME Advantages: Yielding Real-World Gains

SMEs deploying these lines report smoother working capital cycles, funding expansions without equity dilution. In supply chains, tokenized invoices cascade liquidity upstream, stabilizing suppliers. I've witnessed this in Korean ecosystems, where BDACS's KRW1 stablecoin on Plume unlocks local RWA flows. Globally, McKinsey's payments shift forecasts amplify this, with stablecoins handling cross-border settlements at pennies per transaction.

Ondo’s $USDY adds yield accrual, turning idle collateral productive. Bitget flags Centrifuge tokens as 2026 watches, underscoring market conviction.

Platforms revolutionizing this space, like Smestablescredit. com, tailor RWA-backed lines for SME invoice financing, invoice solutions, and growth funding. Their model leverages blockchain rails for transparent, low-cost access, ideal for Asian hybrids I've long championed.

As 2026 unfolds, private on-chain credit eyes trillions, per Orochi Network. SMEs agile enough to integrate these tools will outpace peers mired in legacy friction. The trillion-dollar opportunity beckons those ready to tokenize tomorrow's cash flows today.

No comments yet. Be the first to share your thoughts!