In the fast-paced world of e-commerce, small and medium-sized enterprises (SMEs) often grapple with cash flow bottlenecks tied to unpaid invoices. Traditional financing methods, burdened by lengthy approval processes and high fees, leave many sellers waiting 30 to 90 days for payments from platforms like Amazon or Shopify. This delay hampers inventory restocking, marketing investments, and overall growth. Enter RWA-backed stablecoin lines of credit, a blockchain innovation that tokenizes real-world assets to provide immediate liquidity against verified invoices. Platforms such as Smestablescredit. com are pioneering this space, offering SME e-commerce credit lines that bypass banking inertia while maintaining collateral stability.

Market Surge in Real-World Asset Tokenization Fuels SME Opportunities

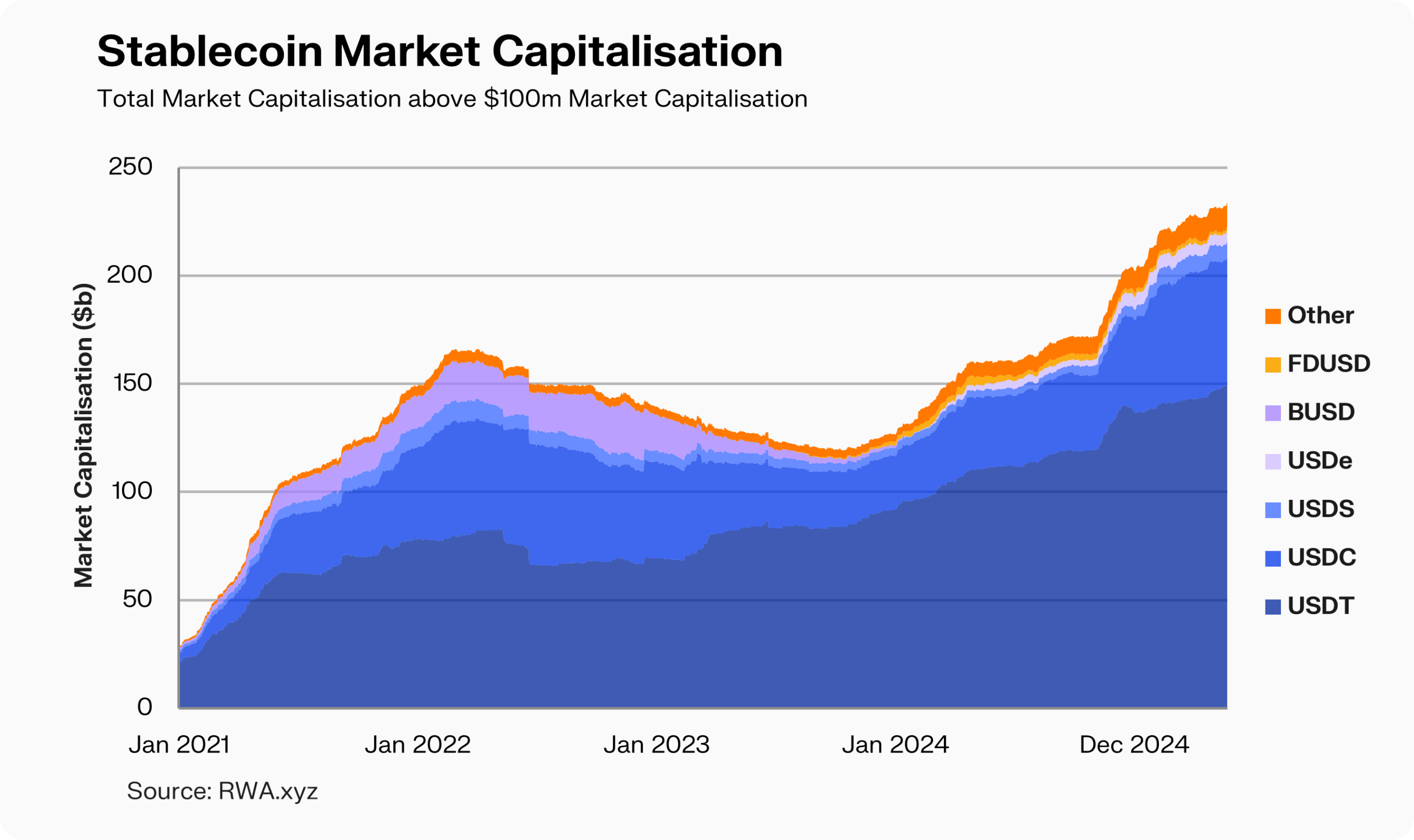

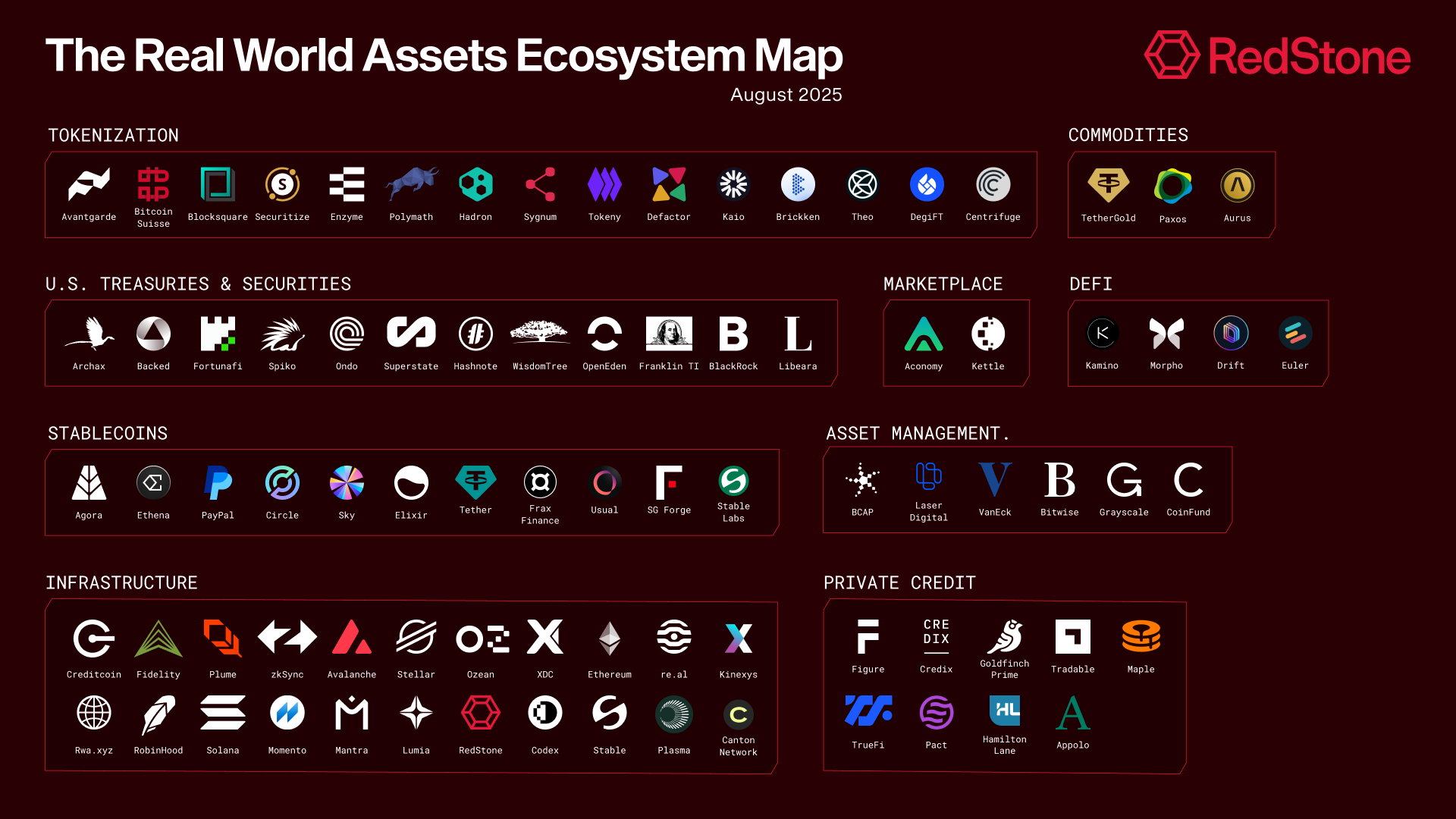

The tokenized real-world asset (RWA) market has witnessed explosive growth, surging approximately 260% in the first half of 2025 alone, from $8.6 billion to over $23 billion in value, according to the RedStone blog's Onchain Finance Report. This expansion underscores a shift toward real world asset SME financing, where invoices, inventory, and receivables become programmable collateral on blockchain networks. Centrifuge. io, a leader in onchain asset management, exemplifies this by providing infrastructure to tokenize and manage RWAs, enabling seamless integration into DeFi protocols.

From a macro perspective, as highlighted in OKX Research, RWAs enhance payment efficiency and collateral utilization, ultimately expanding credit availability. For e-commerce SMEs, this means stablecoin LOC for invoices can unlock working capital without diluting equity or incurring volatile crypto exposure. Conservative investors appreciate the backing of tangible assets, reducing default risks compared to unsecured lending.

Yet, this is no speculative bubble; it's a conservative evolution rooted in fixed-income principles. Tokenization converts passive ledger entries into dynamic, yield-bearing instruments, as systematized in the arXiv SoK on RWA Tokenization. E-commerce operators benefit directly, financing bulk purchases or seasonal spikes with precision.

Why E-Commerce SMEs Need Blockchain Invoice Financing Now

E-commerce trade finance diverges sharply from corporate models, as noted by LinkedIn contributor Ali Amirliravi. SMEs face unique hurdles: fragmented supply chains, variable order volumes, and platform-specific payment terms. Traditional banks demand extensive documentation and collateral, often excluding micro-merchants. In contrast, blockchain invoice financing e-commerce leverages smart contracts for automated verification and disbursement.

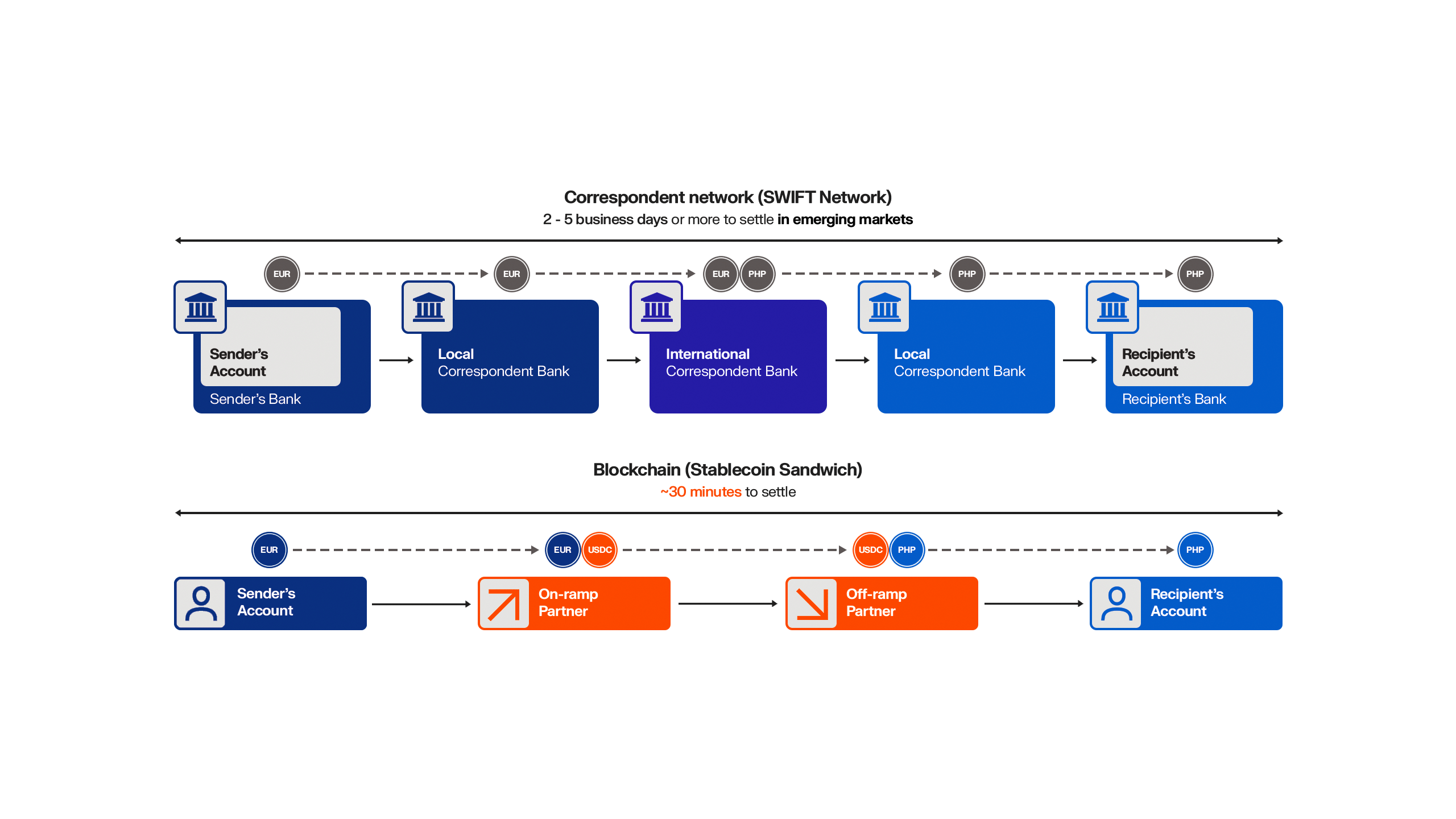

Consider a typical scenario: an SME sells $50,000 in goods via an online marketplace, with net-60 terms. Conventional factoring might charge 2-5% fees and take weeks. RWA-backed stablecoins, disbursed via USDC or similar, offer near-instant access at fractions of the cost, backed by tokenized receivables. This stability-first approach aligns with my 15 years in fixed-income markets, prioritizing capital efficiency over hype.

Key Advantages for E-Commerce SMEs

- Faster Funding: Platforms like Gladefinance provide instant stablecoin-based invoice financing, skipping traditional bank delays of weeks.

- Lower Costs: Tokenization reduces intermediaries and overhead, as in Credefi’s RWA-collateralized SME lending in the EU.

- Global Accessibility: Borderless stablecoin credit lines enable e-commerce SMEs worldwide, via platforms like Via.

- Asset-Backed Security: RWAs like invoices provide verifiable collateral; Bulla Network reports $6M financed with 100% repayment.

- Automated Compliance: Blockchain smart contracts handle KYC and reporting, as powered by Centrifuge infrastructure.

Platforms like those powered by Centrifuge streamline uploads of verified invoices, instantly appraising value against RWA pools. The result? SMEs maintain operations without the red tape, rocketing toward sustainable growth as touted by Smestablescredit. com's 2026 guide.

Spotlight on Leading Platforms Transforming SME Credit

A constellation of innovators is bridging TradFi and DeFi for e-commerce invoice financing. Gladefinance. co delivers AI-driven stablecoin solutions for importers and exporters, while Credefi. io targets EU SMEs with real estate-collateralized crypto lending. Aionfi. com extends asset-based lines against invoices, and RAAC. io facilitates on-chain borrowing backed by precious metals and real estate.

Further afield, Indentura. com unlocks stablecoin credit facilities adhering to traditional underwriting, and Via. xyz provides borderless business accounts with tailored lines. Bulla Network stands out, having financed over $6 million in freight invoices with 100% repayment over 18 months. Oblixcore. com digitizes B2B receivables for early stablecoin payments, exemplifying efficiency.

Traditional vs RWA-Backed Stablecoin Invoice Financing

| Aspect | Traditional Financing | RWA-Backed Stablecoin Financing |

|---|---|---|

| Speed ⏱️ | Days (30-90) | Hours ⚡ |

| Cost 💰 | 2-5% | 0.5-2% |

| Collateral 🔒 | Personal guarantees | Tokenized RWAs |

| Accessibility 🌍 | Banks only | Global (e.g., Gladefinance, Credefi) |

| Risk ⚠️ | High default | Asset-backed |

Partnerships like Zignaly-ABHI and SILQFi-Helix introduce yield products and Shariah-compliant options, channeling stablecoin capital into SME receivables. Liquid Credit embeds credit rails into payments, streamlining cross-border flows. These developments signal a maturing ecosystem, where conservative risk management meets blockchain scalability for e-commerce resilience.

Adopting these solutions requires a measured approach, balancing innovation with prudent risk assessment. For e-commerce SMEs, the key lies in selecting platforms that prioritize verified asset backing and transparent on-chain auditing, ensuring lines of credit remain resilient amid market fluctuations.

Step-by-Step Path to Securing Stablecoin LOCs

This structured process, honed by platforms like Smestablescredit. com, minimizes friction while maximizing capital velocity. In my experience advising fixed-income strategies, such automation echoes the efficiency of collateralized debt obligations, but with blockchain's immutable transparency. E-commerce operators can thus finance inventory replenishment within hours, not weeks, sustaining competitive edges in volatile retail landscapes.

Take Bulla Network's track record: over $6 million financed in shipping invoices with perfect repayment. This isn't luck; it's the power of stablecoin liquidity pools matched against tokenized trade assets. Similarly, OblixCore's blockchain records enable early payments on B2B invoices, slashing days-sales-outstanding metrics that plague traditional e-commerce cash flows.

Yet conservatism demands scrutiny of counterparty risks. While RWAs mitigate volatility, platform solvency and oracle accuracy for asset valuation remain critical. Diversifying across providers like Gladefinance for AI insights or Credefi for EU-focused receivables hedges these exposures. My fixed-income background underscores the value here: treat stablecoin LOCs as short-duration instruments, rolling them over with yields that often exceed 5-8% annualized, per ecosystem benchmarks.

Risk-Adjusted Returns: A Conservative Lens

Opinionated as I may be, RWA backed stablecoin invoice financing isn't a panacea, but a superior alternative when underwritten properly. Default rates plummet with tokenized collateral, as investors can liquidate RWAs on secondary markets swiftly. Contrast this with unsecured SME loans, where recovery averages under 50%. Partnerships such as Zignaly-ABHI's yield product tie stablecoin holders to SME receivables, creating mutual incentives for repayment and fostering a self-reinforcing credit cycle.

Shariah-compliant innovations from SILQFi-Helix further democratize access, tokenizing invoices for underserved markets without compromising ethical standards. Liquid Credit's embedded rails integrate seamlessly into payment gateways, ideal for cross-border e-commerce where forex fees erode margins. These evolutions affirm a thesis I've long held: blockchain amplifies, rather than replaces, sound financial engineering.

Quantitatively, the 260% RWA market expansion to $23 billion signals institutional inflows, bolstering liquidity for SME e-commerce credit lines. Centrifuge's infrastructure ensures composability, allowing SMEs to layer yield strategies atop basic LOCs. For merchants facing Amazon's net-45 terms, this translates to reinvesting freed capital into ads or suppliers, compounding growth conservatively.

Sustaining Growth in a Tokenized Future

Forward-looking SMEs will embed stablecoin LOC for invoices into core operations, treating them as revolving facilities akin to bank overdrafts, but global and asset-secured. Platforms like Via. xyz and Indentura. com adhere to legacy underwriting, blending familiarity with blockchain speed. RAAC's precious metal backing adds an orthogonal stability layer, appealing to risk-averse operators.

Key Stats on RWA Tokenization Market Growth, SME Invoice Financing Volumes, and E-Commerce Applications

| Category | Metric | Value | Details/Source |

|---|---|---|---|

| RWA Tokenization Market Growth | Market Size (Start H1 2025) | $8.6 billion | RedStone blog |

| RWA Tokenization Market Growth | Market Size (End H1 2025) | Over $23 billion | RedStone blog |

| RWA Tokenization Market Growth | Growth Rate | 260% | H1 2025, RedStone blog |

| SME Invoice Financing Volumes | Total Financed (Bulla Network) | $6 million | Over 18 months, Bulla Network |

| SME Invoice Financing Volumes | Repayment Rate (Bulla Network) | 100% | Over 18 months, Bulla Network |

| E-Commerce Applications | Number of Leading Platforms | 12+ | Gladefinance, Credefi, Aion, RAAC, Indentura, Via, Legasi, Bulla Network, OblixCore, etc. (2026 context) |

Ultimately, real world asset SME financing via blockchain closes the $2.5 trillion global trade finance gap, starting with e-commerce's invoice-heavy workflows. Legasi. io's fiat lines secured by digital assets complement this, avoiding liquidation pitfalls. As adoption scales, expect refined oracles, regulatory clarity, and hybrid models marrying TradFi guarantees with DeFi efficiency.

E-commerce SMEs poised to thrive will prioritize platforms with proven repayment histories and diversified collateral. This stability-first paradigm, bridging my worlds of fixed income and RWAs, equips businesses for enduring success amid economic cycles. The invoice, once a liability, now powers propulsion.

No comments yet. Be the first to share your thoughts!